Problems in Reporting Income Tax Article 21 Without Transaction Counterparty Identity

![]() Nurtiyas, S.E., M.Ak

Aug 3, 2024 03:41

80

0

Nurtiyas, S.E., M.Ak

Aug 3, 2024 03:41

80

0

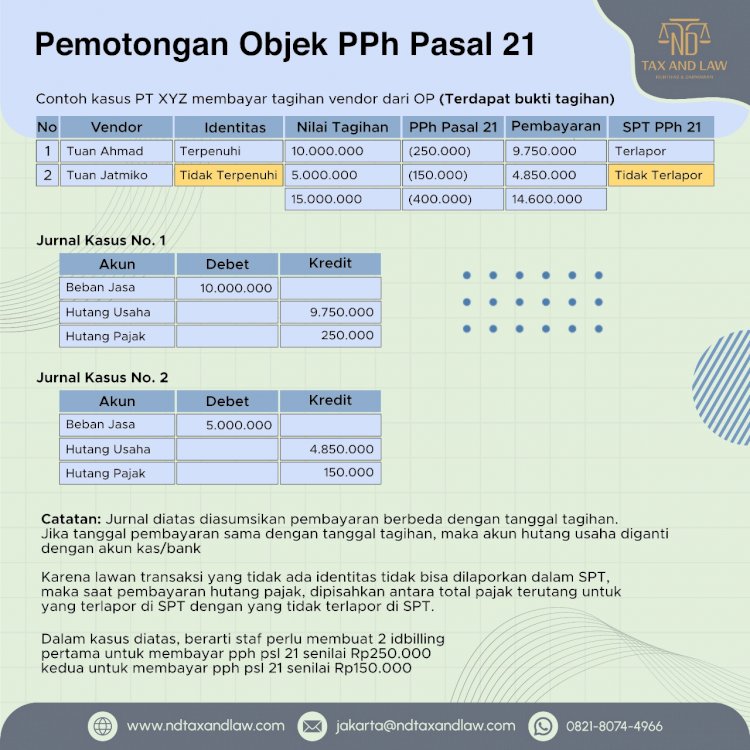

Income Tax (PPh) Article 21 is an important component in the Indonesian taxation system. However, in practice, companies often face obstacles in reporting PPh Article 21, especially when dealing with transactions involving individuals who are unwilling to provide their identity or when the identity provided does not meet tax requirements.

The main problems faced by companies in this situation are:

1. Incomplete data for reporting: Without complete identity from the transaction counterparty, companies cannot fill out the Monthly Tax Return (SPT) for PPh Article 21. Information such as Tax Identification Number (NPWP) or National Identity Number (NIK), and full name are mandatory data that must be reported.

2. Risk of SP2DK and tax audit: The inability to report transactions completely can trigger the issuance of SP2DK (Request for Explanation of Data and/or Information) or even a tax audit.

3. Potential administrative sanctions: Incomplete reporting can result in administrative sanctions in the form of fines or interest. This will certainly be financially detrimental to the company.

4. Difficulties in tax reconciliation: Transactions that are not properly reported can complicate the tax reconciliation process at the end of the year, which in turn can affect the company's overall tax calculations.

To address these issues, some steps that companies can take include:

1. Strengthening internal procedures: Companies need to have a clear policy regarding the necessity of obtaining complete identity from each transaction counterparty before making payments.

2. Educating business partners: Explaining the importance of tax compliance and the legal consequences of non-compliance can help raise awareness among business partners to provide their identity.

3. Consider higher tax withholding: For transactions without complete identity, companies may need to consider applying a higher tax withholding rate in accordance with tax regulations.

4. Good documentation: Even if unable to report transactions completely, companies must still document all efforts made to obtain the identity of the transaction counterparty.

In conclusion, the problem of PPh Article 21 transactions without counterparty identity is a serious challenge for companies in fulfilling their tax obligations. A proactive approach and caution are needed in managing potential risks. Companies need to continuously improve their internal systems and procedures to find solutions that comply with applicable regulations.

For tax consultation and tax disputes, contact us via WhatsApp: 081380935185 (Nurtiyas)